The SEC has been busy, assembly with all the potential issuers of spot Bitcoin ETFs with energetic purposes in December. These conferences have resulted within the common adoption of a money creation methodology by these issuers as an alternative of “in type” transfers, as is typical for different ETFs. A lot has been stated about this modification, starting from the absurd to the intense. The TLDR, nonetheless, is the general impression shall be minimal to traders, comparatively significant to the issuers and it displays poorly on the SEC total.

With the intention to present context, it is very important describe the essential construction of Trade Traded Funds. ETF issuers all interact with a gaggle of Approved Contributors (APs) which have the flexibility to alternate both a predefined quantity of the funds property (shares, bonds, commodities, and so on) or an outlined amount of money or a mixture of each, for a hard and fast quantity of ETF shares for a predetermined price. On this case, had been “in type” creation to be allowed, a reasonably typical creation unit would have been 100 Bitcoin in alternate for 100,000 ETF shares. With money creation, nonetheless, the Issuer shall be required to publish the money quantity, in actual time as the value of Bitcoin modifications, to amass, on this instance, 100 Bitcoin. (In addition they should publish the money quantity that 100,000 ETF shares could be redeemed for in actual time.) Subsequently the issuer is chargeable for buying that 100 Bitcoin for the fund to be in compliance with its covenants or promoting the 100 Bitcoin within the case of a redemption.

This mechanism holds for all Trade Traded Funds, and, as could be seen, implies that the claims that money creation means the fund wont be backed 100% by Bitcoin holding is improper. There might be a really quick delay, after creation, the place the Issuer has but to purchase the Bitcoin they should purchase, however the longer that delay, the extra danger the issuer could be taking. If they should pay greater than the quoted value, the Fund could have a unfavorable money stability, which might decrease the Web Asset Worth of the fund. This may, in fact impression its efficiency, which, contemplating what number of issuers are competing, would possible hurt the issuers skill to develop property. If, however, the issuer is ready to purchase the Bitcoin for lower than the money deposited by the APs, then the fund would have a constructive money stability, which may enhance fund efficiency.

One may surmise, due to this fact, that issuers could have an incentive to cite the money value nicely above the precise buying and selling value of Bitcoin (and the redemption value decrease for a similar motive). The issue with that, is the broader the unfold between creation and redemption money quantities, the broader the unfold that APs would possible quote out there to purchase and promote the ETF shares themselves. Most ETFs commerce at very tight spreads, however this mechanism may nicely imply that a few of the Bitcoin ETF points have wider spreads than others and total wider spreads than they might have had with “in type” creation.

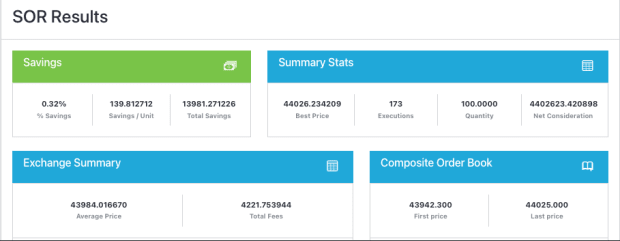

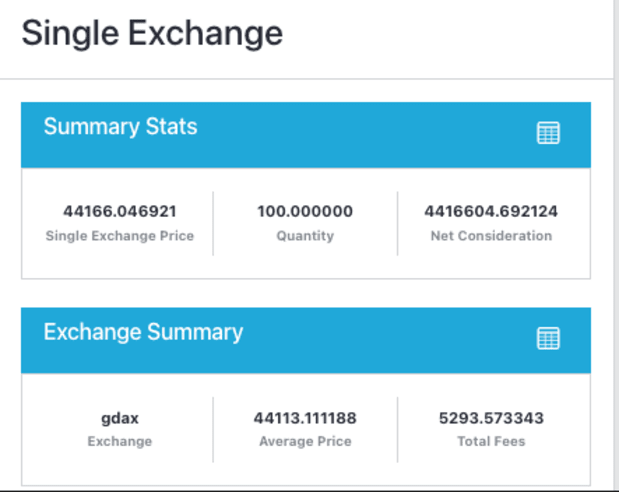

Thus, the issuers should stability the objective of quoting a decent unfold between creation and redemption money quantities with their skill to commerce at or higher than the quoted quantities. This requires, nonetheless, entry to classy know-how to attain. For instance of why that is true, take into account the distinction between quoting for 100 Bitcoin based mostly on the liquidity on Coinbase alone, vis a vis a method that makes use of 4 exchanges which are regulated within the U.S. (Coinbase, Kraken, Bitstamp and Paxos). This instance used CoinRoutes Price Calculator (obtainable by API) which exhibits each single alternate or any customized group of exchanges value to commerce based mostly on full order e-book information held in reminiscence.

In this instance, we see {that a} whole buy value on Coinbase alone would have been $4,416,604.69 however the value to purchase throughout these 4 exchanges would have been $4,402,623.42, which is $13,981.27 costlier. That equates to 0.32% extra expense to purchase the identical 100,000 shares on this instance. This instance additionally exhibits the know-how hurdle confronted by the issuers, because the calculation required traversing 206 particular person market/value stage mixtures. Most conventional monetary techniques don’t must look past a handful of value ranges because the fragmentation in Bitcoin is far bigger.

It’s price noting that it’s unlikely the key issuers will choose to commerce on a single alternate, however it’s possible that some will accomplish that or choose to commerce over-the-counter with market makers that can cost them an extra unfold. Some will choose to make use of algorithmic buying and selling suppliers akin to CoinRoutes or our rivals, that are able to buying and selling at lower than the quoted unfold on common. No matter they select, we don’t anticipate all of the issuers to do the identical factor, that means there shall be doubtlessly vital variation within the pricing and prices between issuers.

These with entry to superior buying and selling know-how will have the ability to provide tighter spreads and superior efficiency.

So, contemplating all of this issue that shall be borne by the issuers, why did the SEC successfully power using Money Creation/Redemption. The reply, sadly, is straightforward: APs, by rule are dealer sellers regulated by the SEC and an SRO akin to FINRA. Up to now, nonetheless, the SEC has not authorized regulated dealer sellers to commerce spot Bitcoin immediately, which they’d have wanted to do if the method was “in type”. This reasoning is a much more easy clarification than varied conspiracy theories I’ve heard, that don’t should be repeated.

In conclusion, the spot ETFs shall be a significant step ahead for the Bitcoin business, however the satan is within the particulars. Traders ought to analysis the mechanisms every issuer chooses to cite and commerce the creation and redemption course of with a purpose to predict which of them may carry out greatest. There are different considerations, together with custodial processes and charges, however ignoring how they plan to commerce might be a pricey choice.

This can be a visitor submit by David Weisberger. Opinions expressed are totally their very own and don’t essentially mirror these of BTC Inc or Bitcoin Journal.